You’ve networked as much as possible, gathered and implemented feedback, and refined your approach—you’re ready to raise your first fund! But, before you can begin pitching LPs, you’ll need a solid deck on hand.

If you’re raising your first private equity fund, you may wonder, “what should be in that deck?” To answer that question, we’ve put together a step-by-step checklist to help your firm assemble a fool-proof deck so you can effectively pitch LPs.

- Start by Setting the Stage

Before diving into the details, it’s a good idea to start your private equity fundraising deck by setting the stage, areas, and locations of where you want to focus your investments.

Are you focused on investing in pre-seed or series B? EdTech or VR? US only or EU? Answer those questions, and show why your focus has value. As an example, if you’re going after VR/AR, explain how the market is projected to grow in revenue over time and the big players that are pioneering growth.

By setting the stage in the first few slides, you’ll make it clear to LPs whether or not you’re aligned with their business goals from the start. - Say What You’re Looking For

Next, share exactly what your firm looks for in a future investment. Do you have clear guidelines when it comes to market potential and valuations? Are you looking for specifics in regard to team members and advisors? Are there clear exit opportunities – like a path to M&A or IPO – that you’re going after? Outline all of that for LPs to know first before diving into the rest of your deck. - Share Your Vision

From core values and mission statements to commonalities between companies you choose to invest in, private equity fundraising places high importance on shared values and visions. Tell LPs precisely what they can expect from you so they can best determine how your brands’ align.

As an example, in Day One Ventures’ fund deck, they clearly outline what the “Day One Spirit” looks like at their firm, which includes:

– Customer Obsession: Great Companies are built around their customer’s needs

– Empathy: Great founders appreciate people and treat everyone daily

– PR Worthy: The company should be at the point where PR and marketing will truly move the needle

By sharing core values from the get-go, you can help LPs determine if you’re the right partner based on goals, ideals, and future visions. - Layout Your Deal-Flow

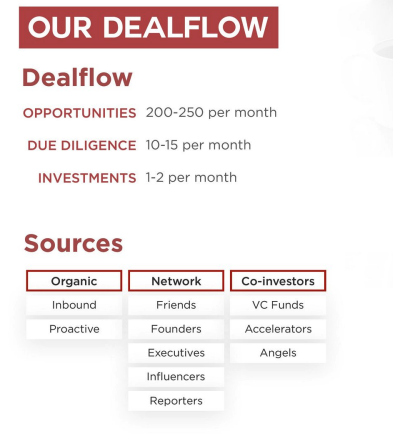

Once LPs have an idea of what a partnership could look like with your firm, it’s time to layout your deal flow in a way that’s easy to follow and comprehend at first glance.

List out specifics, like the number of opportunities you receive each month, how many move forward to due diligence, and how many investments you close. It’s also helpful to include the channels in which you source your deals (organic inbound, network referrals, and co-investors) so LPs know what they’re up against.

Image Source: Day One Ventures’ Fund Deck - Prove Your Value

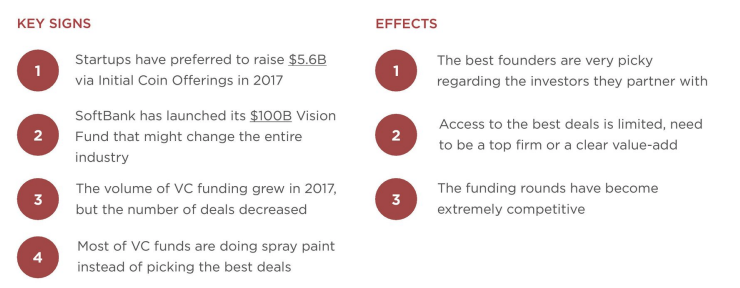

VCs that don’t provide the right value and support can quickly become an unnecessary middleman. Show LPs the value you can add beyond a check by identifying key signs and effects to consider.

If your firm is competitive in the deals you enter, list how, and the effects that can have on the LPs you partner with:

Image Source: Day One Ventures’ Fund Deck

- Show-Off Your High-Quality PR

When looking to secure funding, LPs want to ensure they land an investor that not only understands the importance of PR, but can also help them level up their communications to attract new customers, add value for partners and investors, hire top talent, and more.

If your firm excels in this area, show off a bit here, highlighting examples of press you’ve helped others with, including direct links to stories and features that have driven results. - Outline the Onboarding

LPs want to understand how you’ll help them during onboarding – and this is your chance to tell them what sets your offerings apart.

From learning about business objectives and aligning them to core messaging to providing in-depth media pitching, share what your firm does to take an active role in helping your portfolio members grow. - Focus on the Big Vision

Finally, don’t forget to keep your long-term, “big vision” in mind. Why is your firm in business; what’s your end goal?

Remind LPs of your core purpose so they have a clear understanding of who you are and why you do what you do.

Organize Your Fundraise with Altvia

Getting your deck in a good spot is just the start to a successful first fundraise. Next, you need to quickly identify the right LPs to go after and communicate with them effectively throughout the funnel. Altvia can help.

From organizing a database of high-caliber contacts to providing transparency on tracking, conversions, and communications from deal-sourcing through to value-adding and reporting, Altvia’s software can help supercharge your efforts.

To learn more, get in touch with our team to start a conversation.